- The rise in interest rates saw many investors move into cash.

- Falling inflation and higher starting yields have improved the outlook for bonds.

- Investors should be mindful of the risks associated with tilting or overweighting portfolios in the hunt for growth.

"Appetite for government and high-quality corporate bonds remains strong."

Portfolio Consultant, Vanguard, Europe

The transition to a higher interest rate environment has driven a number of asset allocation trends in client portfolios, based on observations by Vanguard’s Portfolio Analytics & Consulting (PA&C) team.

PA&C is a global team that provides a free portfolio consulting service to advisers as part of Vanguard’s mission to deliver value to investors. We analyse hundreds of client portfolios every year to identify the performance drivers and aggregate exposures across the portfolio, noting any biases, gaps, tilts, concentrations and security overlaps. Our ultimate goal is to help advisers build and maintain portfolios that align with their clients’ goals and attitudes towards risk.

Here we share the three top trends observed across client portfolios over the past year.

The cash trap

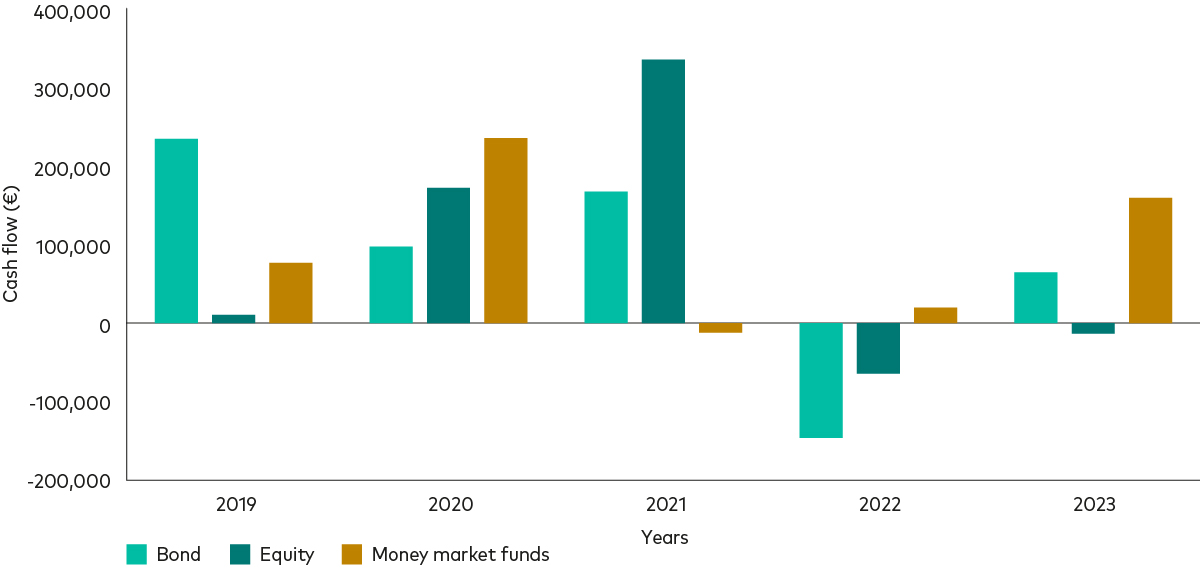

A big theme last year—and in 2022—was the flight to cash. Rates on cash rose as central banks raised interest rates to combat rising inflation. In response, we saw a lot of flows into cash and cash-proxies like money market funds.

While money market funds may at times be a sound location for holding client capital as interest rates rise or as a cash park while deciding how to invest, there are a couple of reasons why going to cash might have put clients further away from their goals.

Firstly, with inflation much higher than savings rates throughout 2023, cash and money market funds were delivering a negative real return. Further, not only did cash fail to match the impacts of inflation, it also posed an opportunity cost, as global equities rose almost 16%1 last year (in nominal terms). Investors that remained invested—particularly in equity markets—would have been better off than those who moved into cash.

Source: Morningstar, includes overseas funds, fund of funds, responsible investments, index trackers. Excludes feeder funds. Flows in EUR. Data from 1 January 2019 to 30 November 2023.

Bonds are back

While many investors allocated to cash in 2023, by the end of the year, flows into bond funds picked up on the back of expectations of interest rate cuts in early 2024. Global bond markets posted their best two-month returns in November and December 2023 since the global financial crisis of 2008, gaining 6.2%2.

The fixed income market rally of late 2023 partly reversed in January 2024 as markets adjusted their interest rate outlook—now more in-line with Vanguard’s long-held view that rate cuts are more likely in the second half of 2024.

While bond prices aren’t as cheap as they were in October 2023, appetite for government and high-quality corporate bonds remains strong, which aligns with our view that interest rates are at peak levels. Rising interest rates caused plenty of short-term pain for multi-asset investors in 2022, but the long-term outlook for bond markets has improved markedly thanks to higher interest rates.

The hunt for growth

Some investors will always be looking for the next big thing or growth opportunities. Vanguard doesn’t advocate tactical tilts and biases, but sometimes we see advisers allocating more to certain regions or sectors in a bid to capture a perceived opportunity. One such trend we’ve seen in the past year or so is advisers adopting an overweight position to emerging market (EM) equities—despite a disappointing decade for EM relative to developed markets.

The underperformance of EM equities over the past decade has left the sub-asset class looking attractive based on current valuations3, which might be a driving factor for those investors tilting client portfolios to EM stocks. While the case can be made for and against EM equities, it’s important that investors understand the higher volatility associated with EM stocks before making any strategic allocation decisions.

In any case, investors can gain exposure to EM equities through a global market capitalisation-weighted index fund, exchange-traded fund (ETF) or model portfolio. If EM stocks do outperform, global equity index exposures will capture those gains without taking on additional risk through an overweight to the sub-asset class. Alternatively, for investors with a preference for active management and a higher tolerance for risk, active EM equity funds seek to generate long-term alpha by investing in companies that operate in developing economies.

Regardless of the implementation, Vanguard advocates a balanced, risk-aware approach to portfolio construction, including any tilts or biases investors may want to express. All of Vanguard’s funds, ETFs and model portfolios—whether index or active—are built with balance and risk in mind.

1 Global equities represented by the ![]() MSCI All Country World Index. Returns calculated in EUR with dividends reinvested. Data between 1 January 2023 and 31 December 2023.

MSCI All Country World Index. Returns calculated in EUR with dividends reinvested. Data between 1 January 2023 and 31 December 2023.

2 Source: Bloomberg, based on total returns for the Bloomberg Global Aggregate Bond Index (USD Hedged) for the period 16 October 2023 to 29 December 2023.

3 Source: Vanguard calculations, based on the Vanguard Capital Markets Model (VCMM). Emerging market equity is represented by MSCI Emerging Markets Total Return Index (EUR).

IMPORTANT: The projections or other information generated by the Vanguard Capital Markets Model® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time. The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include US and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, US money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Some funds invest in emerging markets which can be more volatile than more established markets. As a result the value of your investment may rise or fall.

ETF shares can be bought or sold only through a broker. Investing in ETFs entails stockbroker commission and a bid- offer spread which should be considered fully before investing.

Funds investing in fixed interest securities carry the risk of default on repayment and erosion of the capital value of your investment and the level of income may fluctuate. Movements in interest rates are likely to affect the capital value of fixed interest securities. Corporate bonds may provide higher yields but as such may carry greater credit risk increasing the risk of default on repayment and erosion of the capital value of your investment. The level of income may fluctuate and movements in interest rates are likely to affect the capital value of bonds.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained herein is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information does not constitute legal, tax, or investment advice. You must not, therefore, rely on it when making any investment decisions.

The information contained herein is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

The funds or securities referred to herein are not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds or securities. The prospectus or the Statement of Additional Information contains a more detailed description of the limited relationship MSCI has with Vanguard and any related funds.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited ("BISL") (collectively, "Bloomberg"), or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices.

The products are not sponsored, endorsed, issued, sold or promoted by “Bloomberg.” Bloomberg makes no representation or warranty, express or implied, to the owners or purchasers of the products or any member of the public regarding the advisability of investing in securities generally or in the products particularly or the ability of the Bloomberg Indices to track general bond market performance. Bloomberg shall not pass on the legality or suitability of the products with respect to any person or entity. Bloomberg’s only relationship to Vanguard and the products are the licensing of the Bloomberg Indices which are determined, composed and calculated by BISL without regard to Vanguard or the products or any owners or purchasers of the products. Bloomberg has no obligation to take the needs of the products or the owners of the products into consideration in determining, composing or calculating the Bloomberg Indices. Bloomberg shall not be responsible for and has not participated in the determination of the timing of, prices at, or quantities of the products to be issued. Bloomberg shall not have any obligation or liability in connection with the administration, marketing or trading of the products.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2024 Vanguard Group (Ireland) Limited. All rights reserved.

© 2024 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2024 Vanguard Asset Management, Limited. All rights reserved.